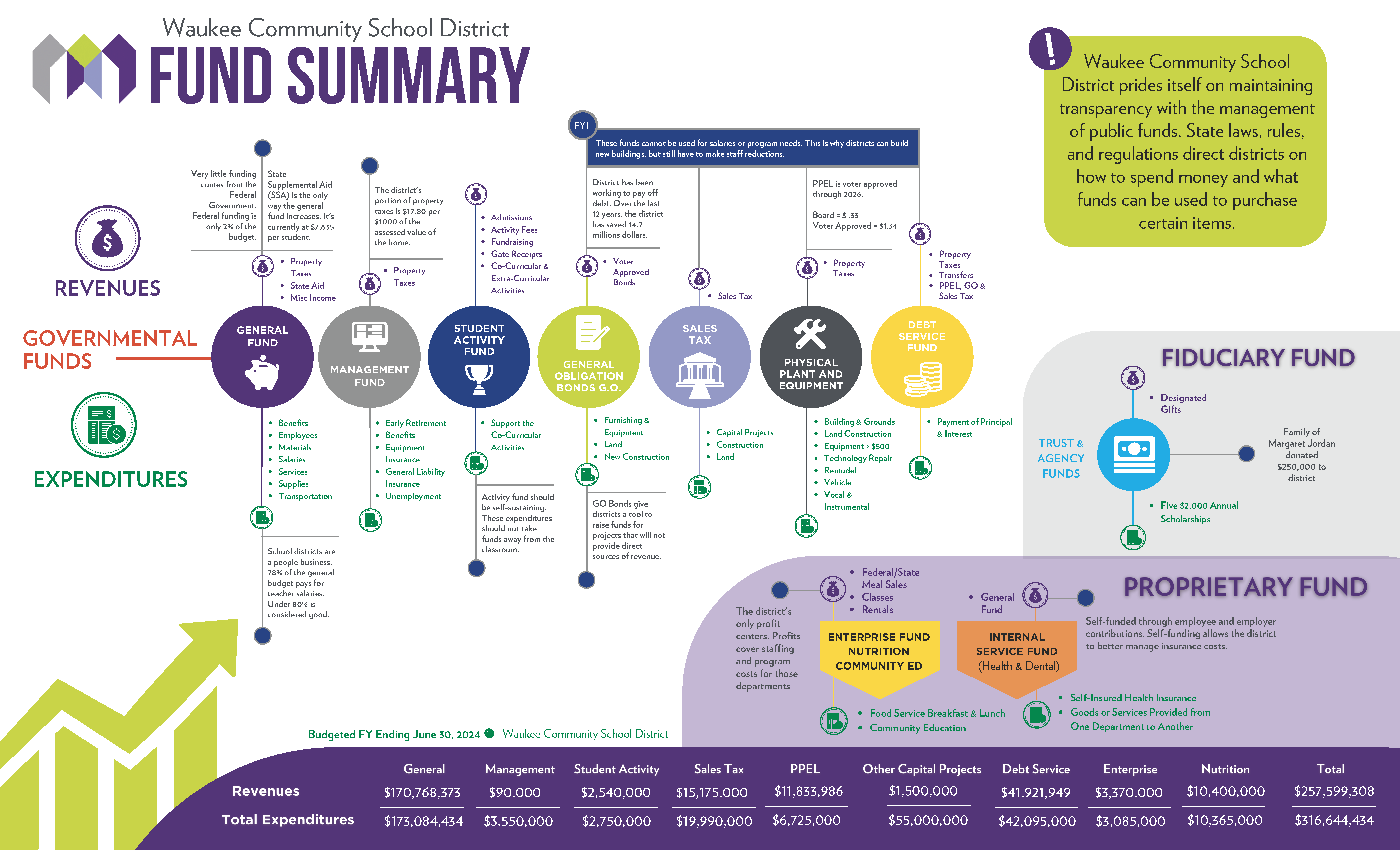

Waukee Community School District prides itself on maintaining transparency with the management of public funds. State laws, rules, and regulations direct districts on how to spend money and what funds can be used to purchase certain items. Below you will find descriptions of the types of funds the district uses and their purposes.

Fund Summary Definitions

Fund 10 – General Fund

This fund receives the revenues from the school finance formula. It is a governmental fund under GAAP (generally accepted accounting principles) and accounts for the revenues and expenditures for the educational program and most school district operations. All money received by a school corporation from taxes and other sources must be accounted for in the General Fund except money required by law to be accounted for in another fund. Expenditures include employee salaries and benefits (except nutrition and community education), textbooks, tuition, open enrollment, supplies, contracted services, travel, etc.

Fund 21 – Student Activity Fund

Money from student-related activities such as admissions, activity fees, student dues, student-fundraising events, or other student-related co-curricular or extracurricular activities is deposited in this fund. Expenditures for interscholastic athletics, student councils, clubs, and other student activities are in this fund.

Fund 22 – Management Fund

This fund is supported by a property tax levy used for early retirement, unemployment, tort liability, and insurance. This fund may be used for equipment breakdown insurance and may join and pay funds into a local government risk pool to protect against liability. The district belongs to the Iowa Association of School Board’s Safety Group that provides insurance on vehicles, buildings, errors, and omissions, etc.

Fund 31 – General Obligation (G.O.) Bonds

This fund accounts for expenditures funded by governmental obligation bonds to be used to build and equip new facilities. This fund cannot be used for salaries or programs needs.

Fund 33 – Statewide School Infrastructure Sales and Services Tax (Sales Tax) Fund

This fund accounts for the revenue and expenditures connected to the statewide sales tax for a school district. Funds may be used for the same purpose as Capital Projects Fund and PPEL Fund and include construction of buildings, purchasing property, equipment, technology, etc. This fund cannot be used for salaries or programs needs.

Fund 36 – PPEL (Physical Plant Equipment Levy) Fund

This fund is a capital project fund providing a maximum of $1.67 per $1,000 of assessed valuation. The board may approve 33 cents annually in property tax; and/or hold an election for up to $1.34 for a period of up to 10 years and funded by property tax or property tax and income surtax. Funds may be used for the same purpose as Capital Projects Fund and Sales Tax Funds and include construction of buildings, purchasing property, equipment, technology, etc. This fund cannot be used for salaries or programs needs.

Fund 40 – Debt Fund

Voters may approve bonded indebtedness for a period of up to twenty years and a rate limit up to $4.05 per thousand dollars of assessed valuation. The debt levy revenue is used to pay the interest, interest, and indebtedness costs. Money available to service this debt and received from other sources are transferred to the debt service fund and the payment is then made from this fund. This fund cannot be used for salaries or programs needs.

Fund 61 – Nutrition Fund

This fund accounts for revenues and expenditures connected with operating the District’s lunch and breakfast programs. All 6X funds are enterprise funds used to account for operations that are operated in a similar manner to private business where revenues are based on fees charged and expenses are directly associated with the operations.

Fund 65 – Community Education Fund

This fund accounts for revenues and expenditures connected with transactions for the district’s before and after-school child care and summer child care programs, facilities, and services to provide further education opportunities to the local area. All 6X funds are enterprise funds used to account for operations that are operated in a similar manner to private business where revenues are based on fees charged and expenses are directly associated with the operations.

Fund 71, 72, 73 – Internal Service Fund

This fund accounts for transactions for self-insured insurances including medical, dental, prescription, and vision received by district employees for whom the district is responsible for paying all claims and administrative costs. This fund also accounts for transactions for certain benefits available to district employees in which the District is responsible for paying all premiums or costs specified by the employee.

Fund 81, 82, 84 – Trust & Agency Funds

These are fiduciary funds that were donated to the district. Interest earned from the trust allows the district to award five $2,000 scholarships to students each year.